The maritime transport is the key pillar of the international trade and global economy. Over 80% by volume and 70% by value of international trade represent Maritime trade. In Myanmar as well, Maritime trade is the backbone of international trade and country economy. All ports of Myanmar are administered by single organization Myanma Port Authority (MPA) under the supervision of Ministry of Transport and Communications and MPA is responsible for the monitoring and facilitating policies of the country economy and the ministry to facilitate trade and the seamless flow of goods. Law, Rules and regulations regarding port operation and management...

See More

Highlighted New

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်တင်သွင်းနိုင်ရန်အတွက်လည်းကောင်း၊ ကုန်သေတ္တာသင်္ဘောလိုင်းအသီးသီးမှ ခရီးစဉ်များပြန်လည် တိုးချဲ့ပြေးဆွဲရန် စီစဉ်ထားရှိသဖြင့် ဧပြီလတွင်...

Read More|

( 15-4-2024 11:00 AM To 22-4-2024 11:00 AM ) Market Trading

|

|---|

| 1 USD = 3311.00MMK |

| View All |

|

|

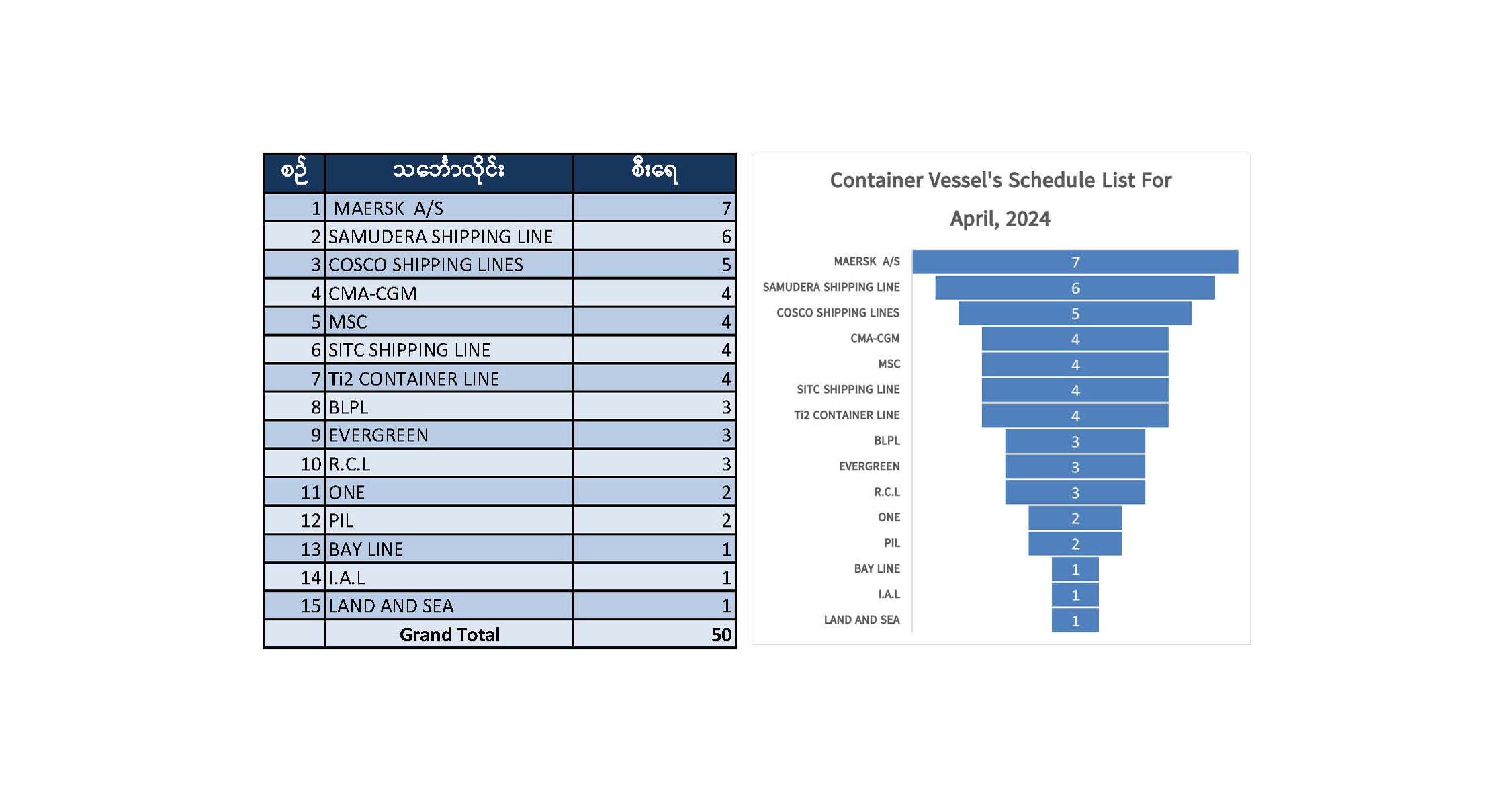

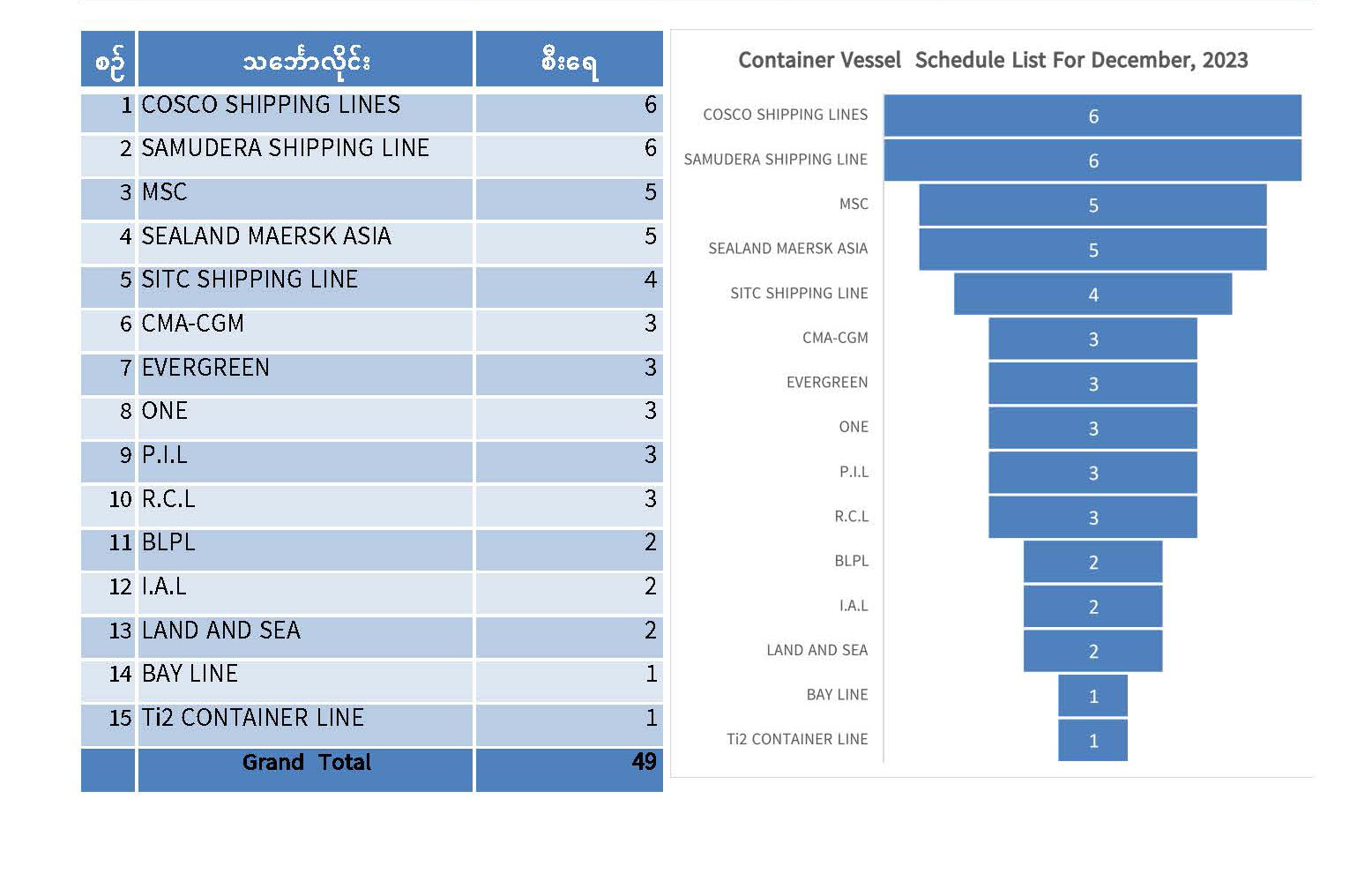

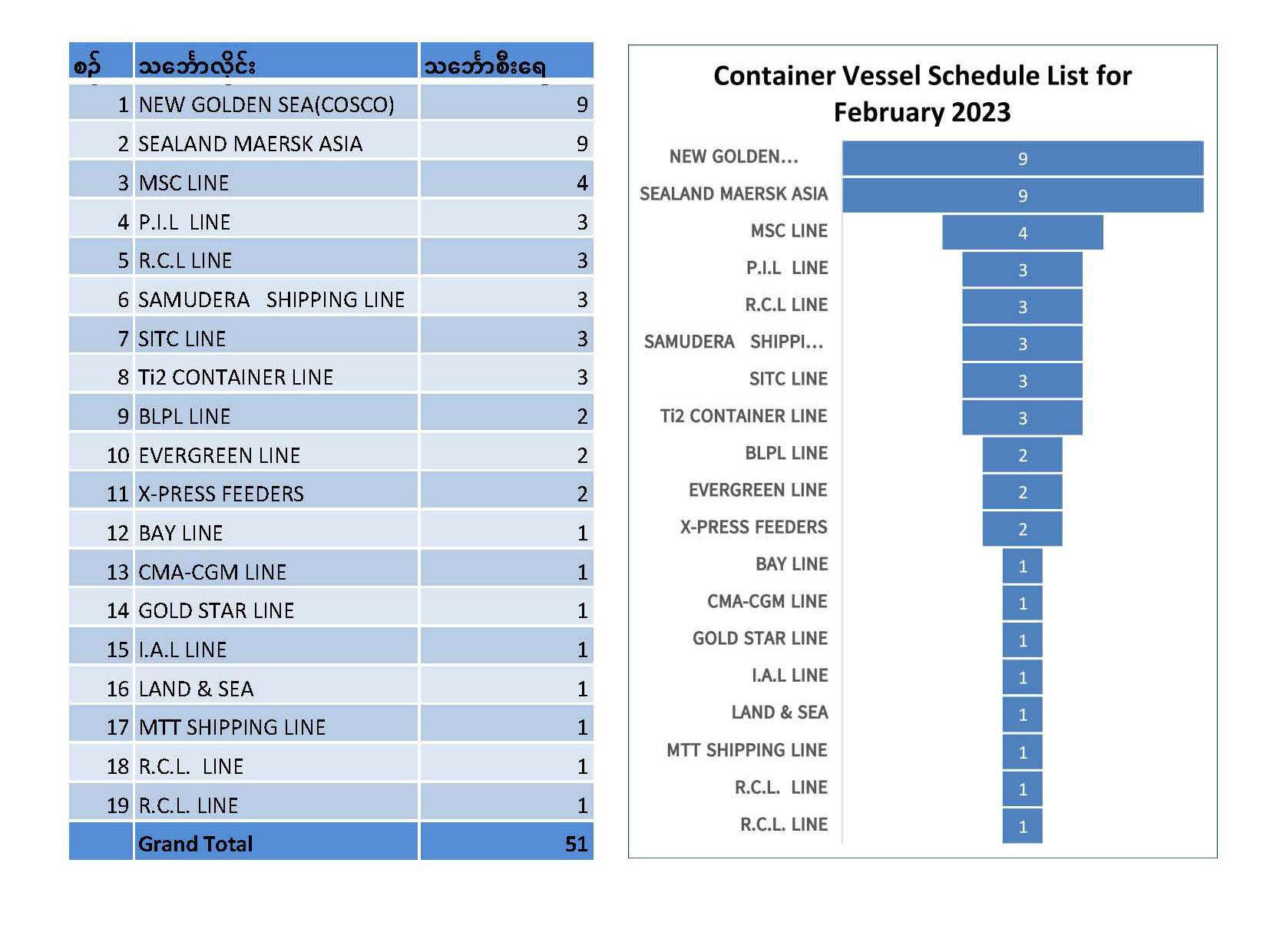

၂၀၂၄ ခုနှစ်၊ ဧပြီလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်တင်သွင်းနိုင်ရန်အတွက်လည်းကောင်း၊... |

March 29, 2024 |

2024 | Mar |

|

ပွင့်လင်းရာသီ ရန်ကုန်ဆိပ်ကမ်း၌ ပြည်ပသို့ ဆန်၊ ပဲ၊ ပြောင်း တင်ပို့မည့် သင်္ဘောကြီးများဖြင့် စည်ကားလျက်ရှိ |

ရန်ကုန်၊ မတ် ၅ မြန်မာနိုင်ငံသည်... |

March 5, 2024 |

2024 | Mar |

|

နိုင်ငံတော်စီမံအုပ်ချုပ်ရေးကောင်စီအဖွဲ့ဝင်၊ ဒုတိယဝန်ကြီးချုပ်နှင့် ပို့ဆောင်ရေးနှင့်ဆက်သွယ်ရေးဝန်ကြီးဌာန ပြည်ထောင်စုဝန်ကြီး ဗိုလ်ချုပ်ကြီး မြထွန်းဦး တက်ရောက်ချီးမြှင့်ခဲ့သည့် မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်မှ ၆၀မီတာ ဘက်စုံသုံး ဗော်ယာ မ/ချ ရေယာဉ်(၁)စီး၊ မြေတူးမြေခံ ရေယာဉ်(၂)စုံနှင့် ဆိပ်ကမ်းလုပ်ငန်းသုံး ရေယာဉ်(၃)စီး စုစုပေါင်း ရေယာဉ်(၈)စီး လုပ်ငန်းခွင် စတင်ဝင်ရောက်ခြင်း အခမ်းအနားသို့ တက်ရောက် အမှာစကားပြောကြား |

ပို့ဆောင်ရေးနှင့်ဆက်သွယ်ရေးဝန်ကြီးဌာန၊ မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်တွင် ၆၀ မီတာ ဘက်စုံသုံး... |

March 4, 2024 |

2024 | Mar |

|

နိုင်ငံတော်စီမံအုပ်ချုပ်ရေးကောင်စီ အဖွဲ့ဝင်၊ ဒုတိယဝန်ကြီးချုပ်နှင့် ပို့ဆောင်ရေးနှင့် ဆက်သွယ်ရေးဝန်ကြီးဌာန ပြည်ထောင်စုဝန်ကြီး ဗိုလ်ချုပ်ကြီး မြထွန်းဦး ရန်ကုန်မြို့ရှိ မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်၊ ဆူးလေအပြည်ပြည်ဆိုင်ရာဆိပ်ကမ်းတံတားတွင် ပြည်ပတင်ပို့ရန် ဆန်တင်လုပ်ငန်းဆောင်ရွက်နေမှုနှင့် သိုလှောင်ရုံများ ပြုပြင်မွမ်းမံခြင်း ဆောင်ရွက်နေမှု အခြေအနေများအား ကြည့်ရှုစစ်ဆေး |

နိုင်ငံတော်စီမံအုပ်ချုပ်ရေးကောင်စီဝင်၊ ဒုတိယဝန်ကြီးချုပ်နှင့် ပို့ဆောင်ရေးနှင့် ဆက်သွယ်ရေး ဝန်ကြီးဌာန၊... |

March 4, 2024 |

2024 | Mar |

|

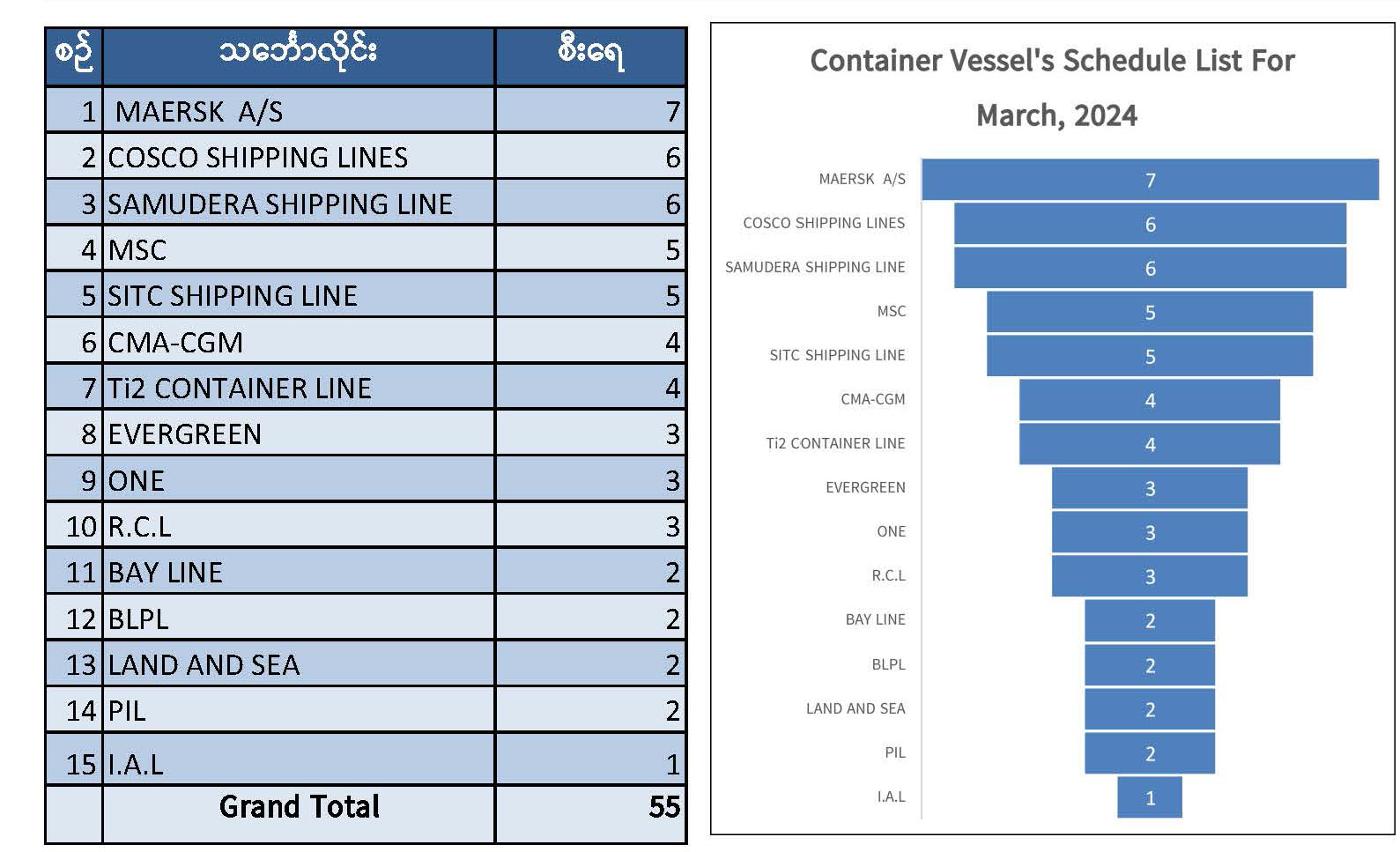

၂၀၂၄ ခုနှစ်၊ မတ်လအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်တင်သွင်းနိုင်ရန်အတွက်လည်းကောင်း၊ကုန်သေတ္တာသင်္ဘောလိုင်းအသီးသီးမှခရီးစဉ်များပြန်လည်... |

February 28, 2024 |

2024 | Feb |

|

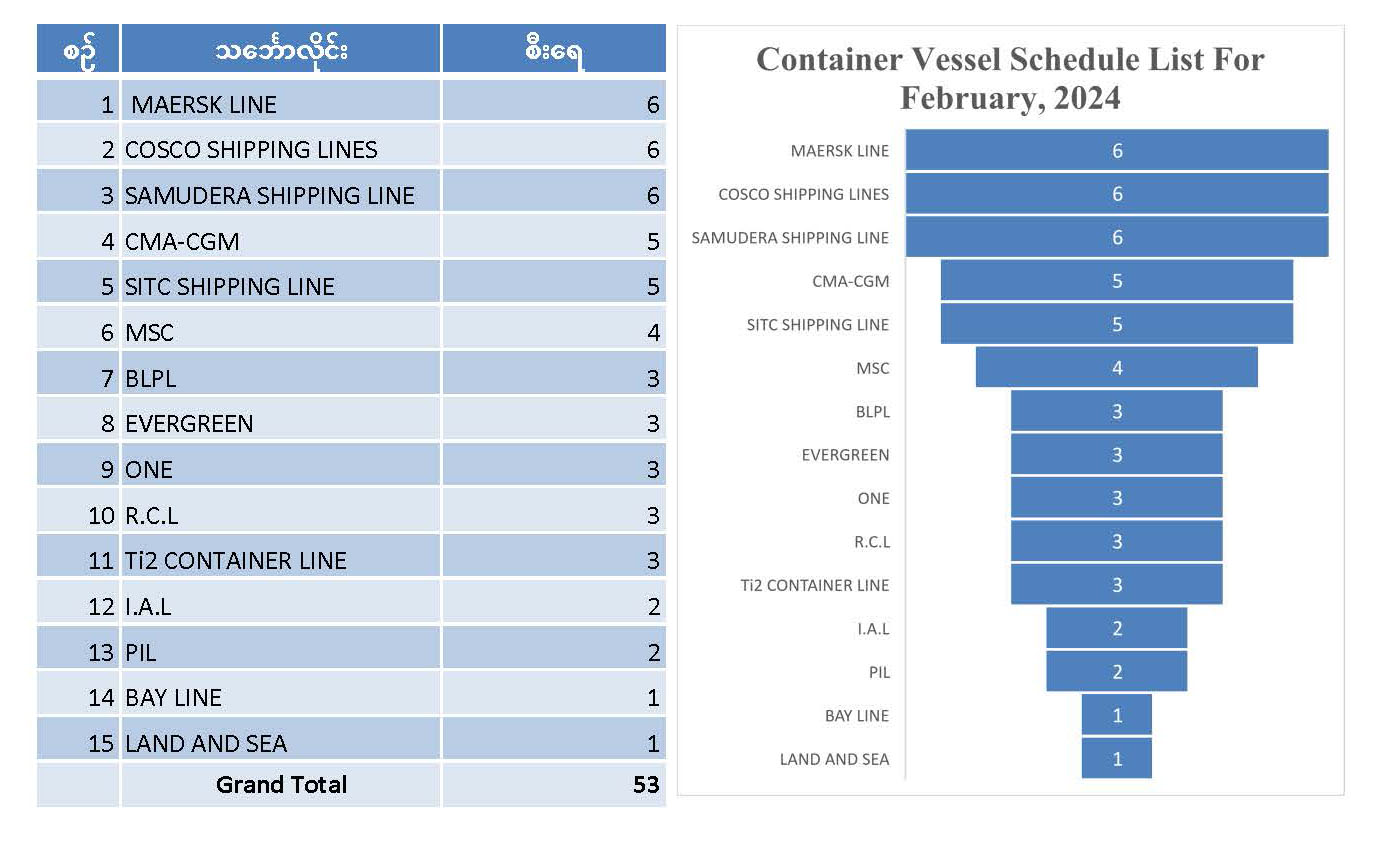

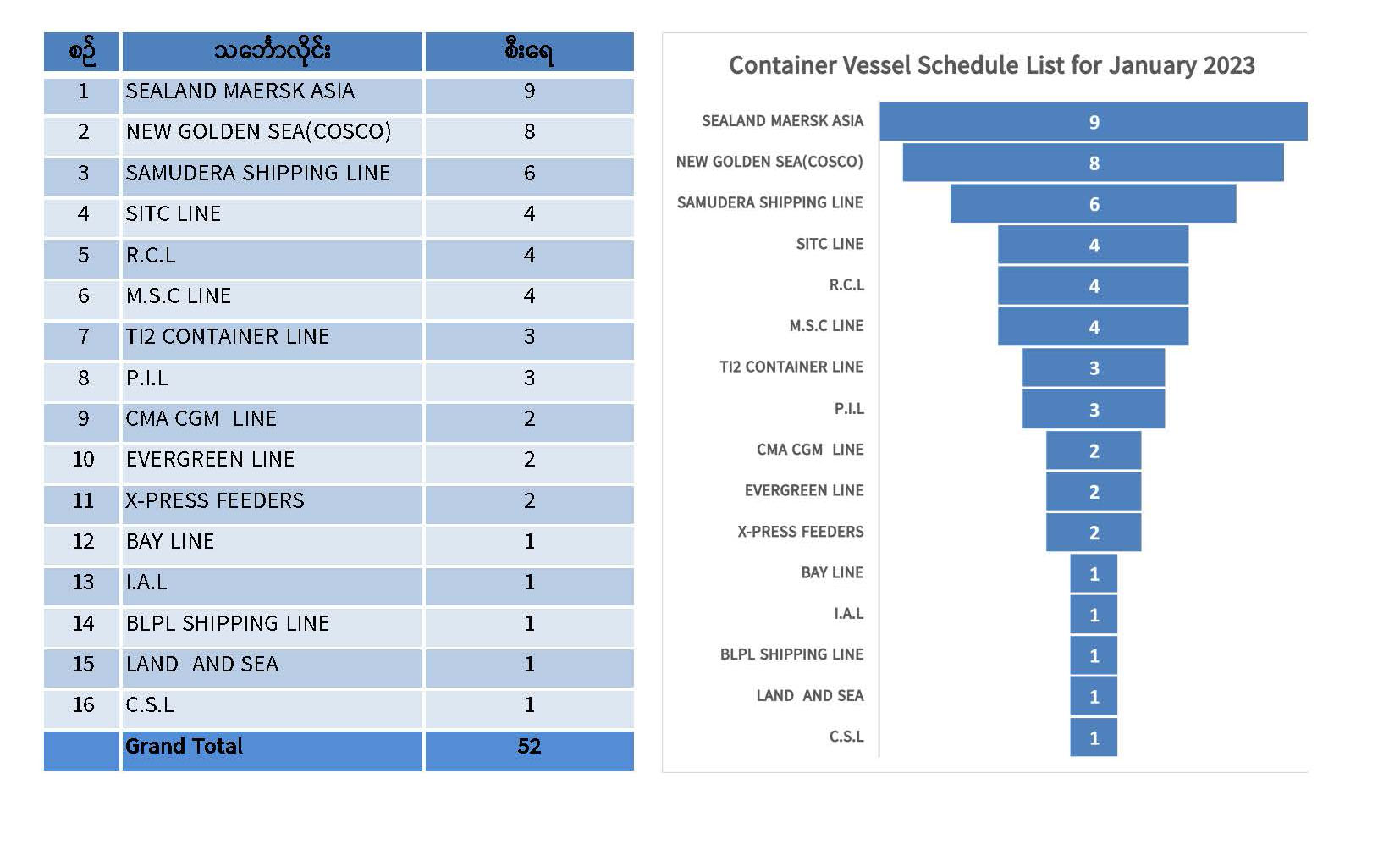

၂၀၂၄ ခုနှစ်၊ ဖေဖေါ်ဝါရီလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်တင်သွင်းနိုင်ရန်အတွက်လည်းကောင်း၊ကုန်သေတ္တာသင်္ဘောလိုင်းအသီးသီးမှခရီးစဉ်များ... |

Janauary 31, 2024 |

2024 | Jan |

|

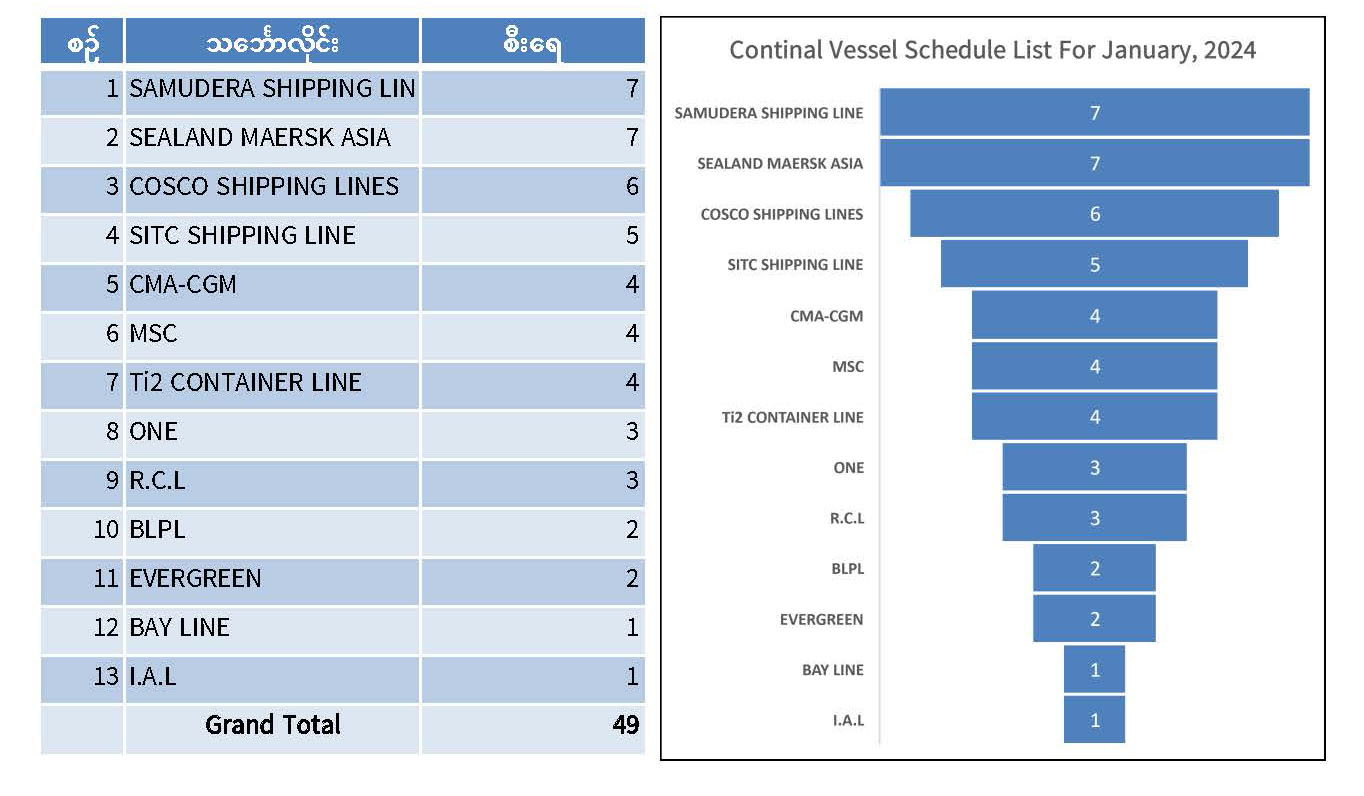

၂၀၂၄ ခုနှစ်၊ ဇန်နဝါရီလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များ လည်း... |

December 29, 2023 |

2023 | Dec |

|

၂၀၂၃ ခုနှစ်၊ ဒီဇင်ဘာလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များ လည်း... |

November 29, 2023 |

2023 | Nov |

|

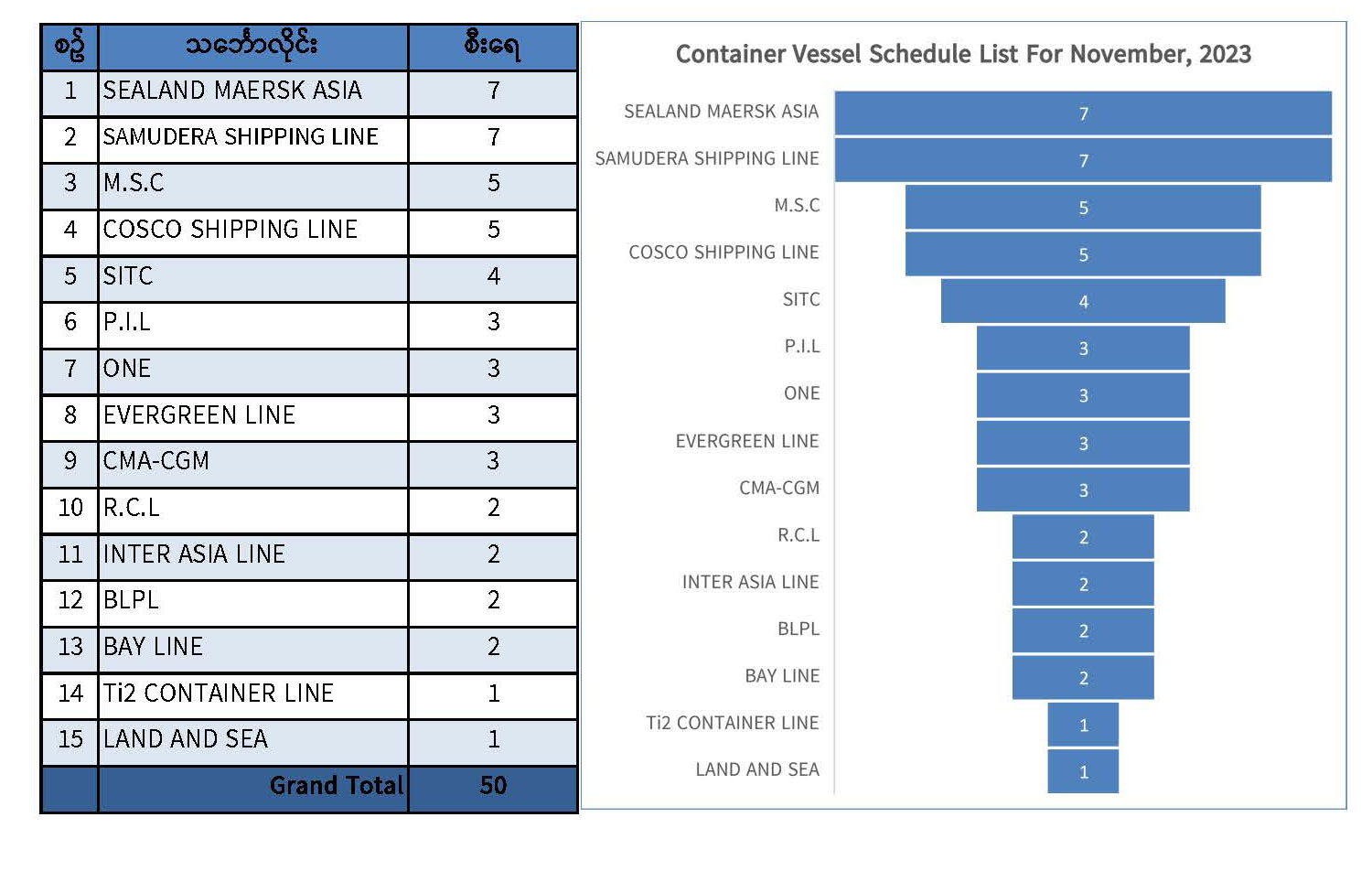

၂၀၂၃ ခုနှစ်၊ နိုဝင်ဘာလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

October 31, 2023 |

2023 | Oct |

|

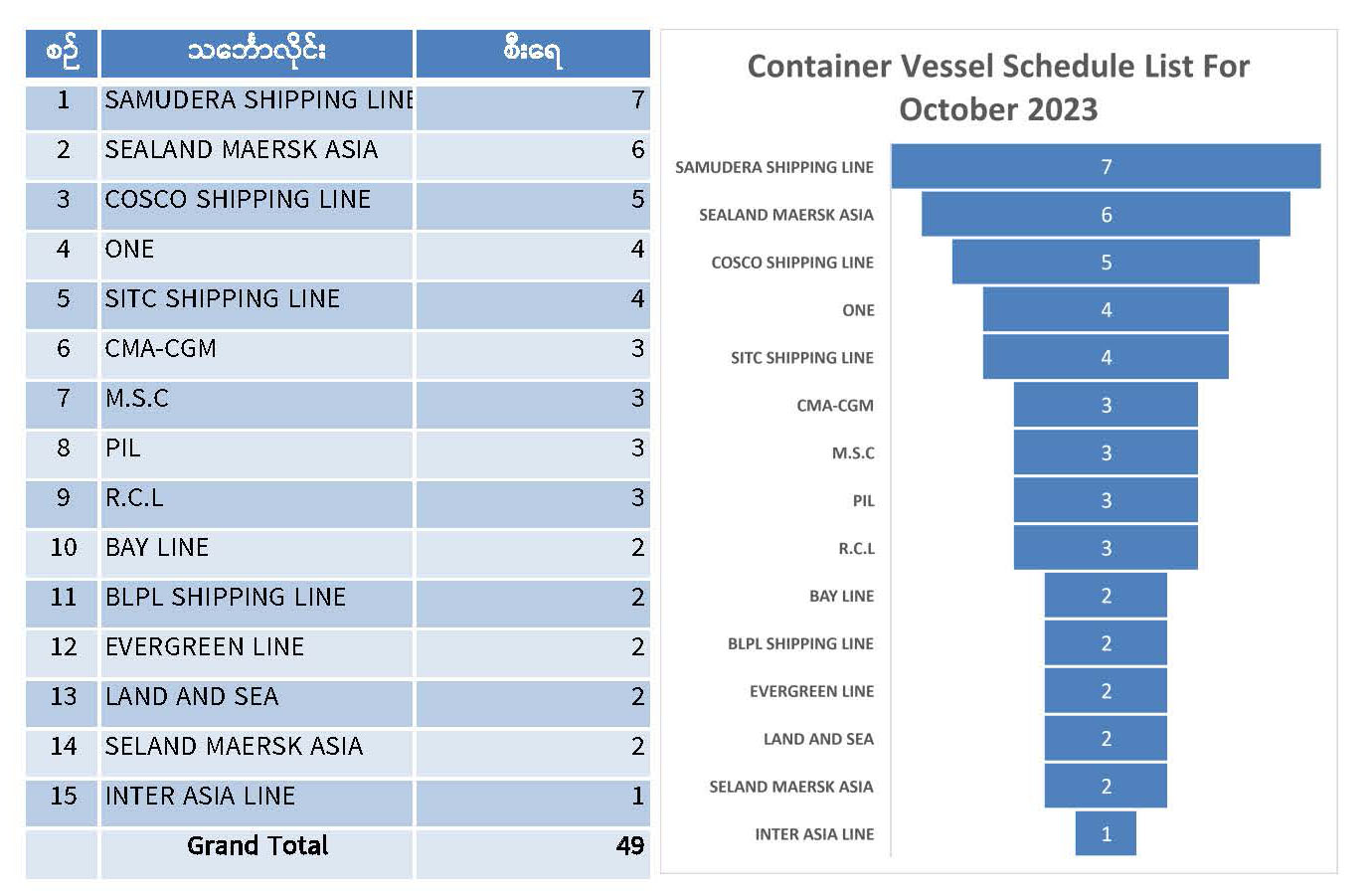

၂၀၂၃ ခုနှစ်၊ အောက်တိုဘာလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

October 2, 2023 |

2023 | Oct |

|

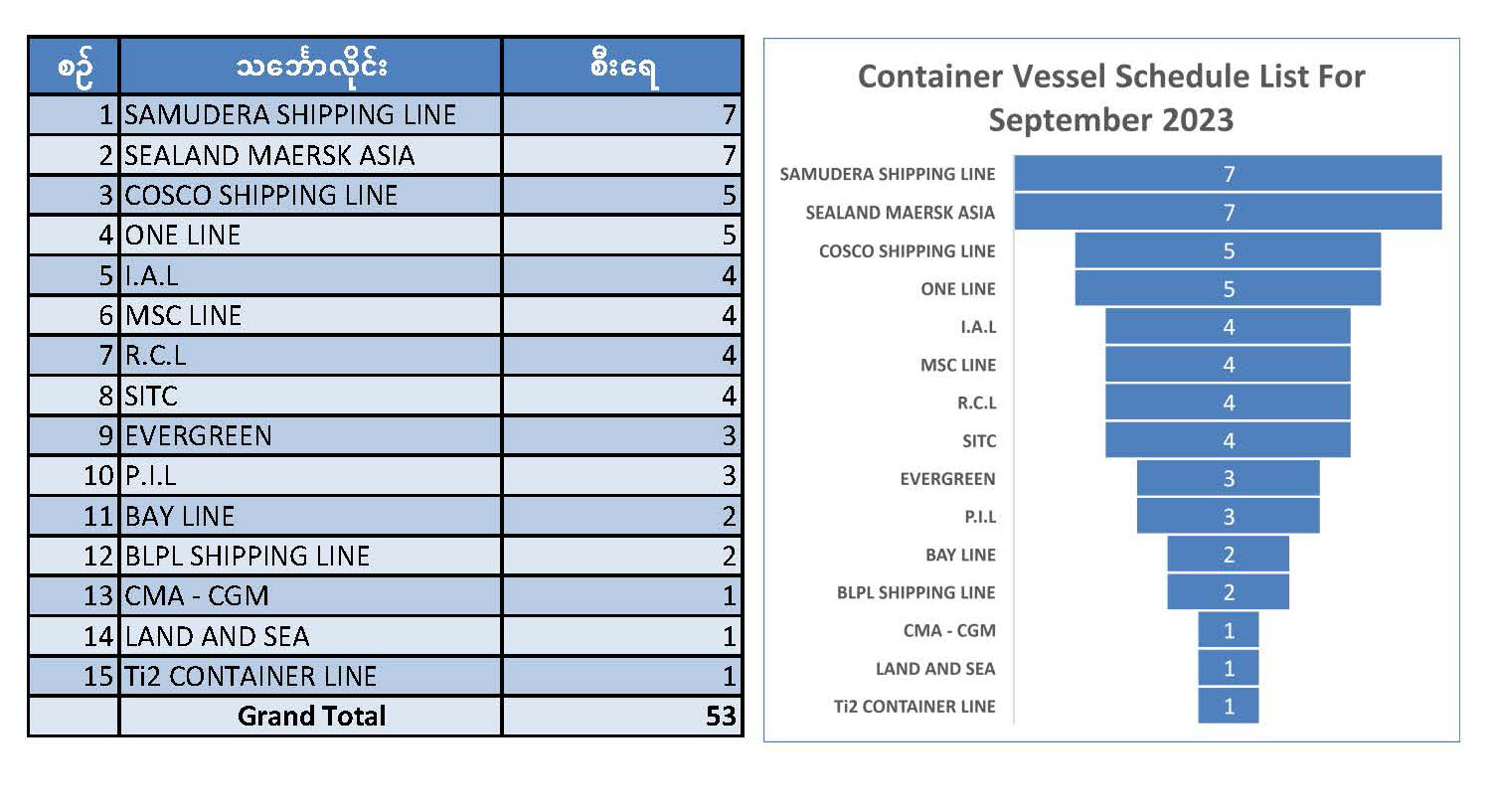

၂၀၂၃ ခုနှစ်၊ စက်တင်ဘာလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

August 30, 2023 |

2023 | Aug |

|

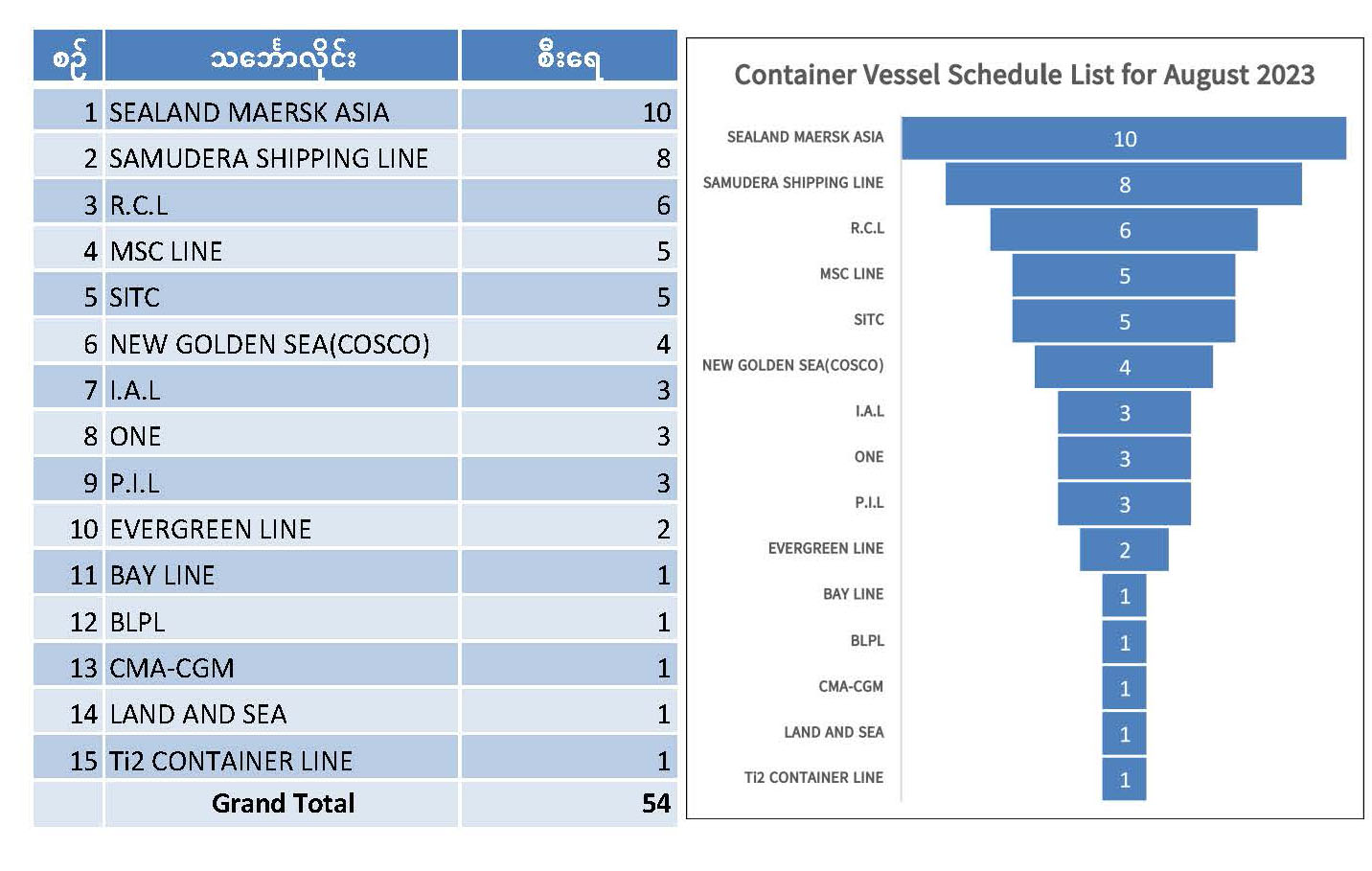

၂၀၂၃ ခုနှစ်၊ ဩဂုတ်လအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

July 28, 2023 |

2023 | Jul |

|

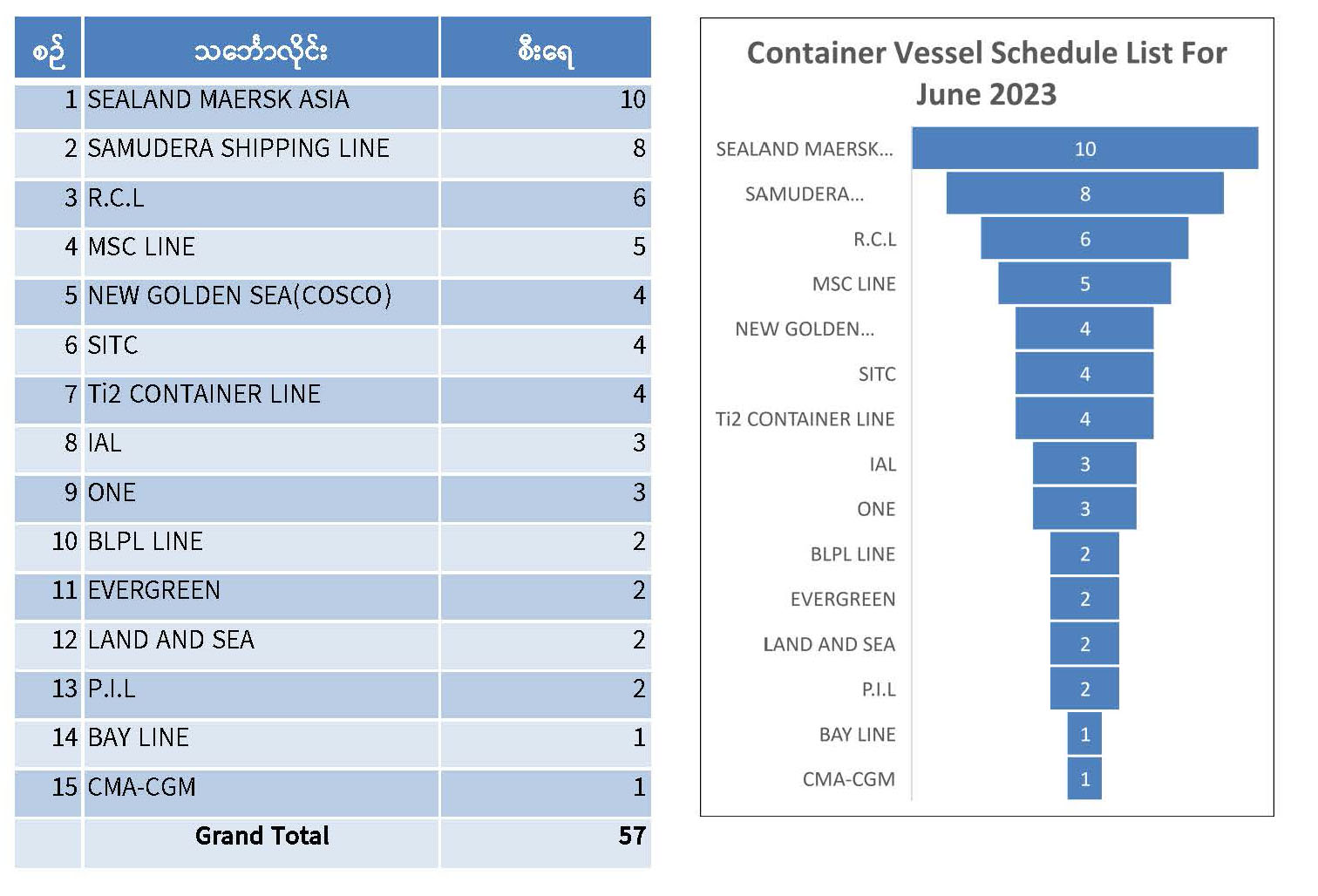

၂၀၂၃ ခုနှစ်၊ ဇူလိုင်လအတွက် ကုန်သေတ္တာတင်သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

no 30, 2023 |

2023 | Jun |

|

ရေလမ်းကြောင်တိုးတက်ကောင်းမွန်လာသည်နှင့်အမျှ ရန်ကုန်အတွင်း ဆိပ်ကမ်းဧရိယာရှိ ဆိပ်ကမ်းတံတားများမှ အရွယ်အစားကြီးမားသော ကုန်သေတ္တာသင်္ဘောကြီးများကို လက်ခံ ဝန်ဆောင်မှုပေးလာနိုင် |

ရန်ကုန် ၂၂ ပို့ဆောင်ရေးနှင့်ဆက်သွယ်ရေးဝန်ကြီးဌာန၊ မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်သည် ရန်ကုန်အတွင်း... |

no 26, 2023 |

2023 | Jun |

|

ရခိုင်ပြည်နယ်ကယ်ဆယ်ရေးနှင့်ပြန်လည်ထူထောင်ရေးလုပ်ငန်းများ ဆောင်ရွက်နိုင်ရန်အတွက် TMT ဆိပ်ကမ်းတံတားမှ စစ်တွေမြို့ရှိ ဆိပ်ကမ်းများသို့ ဌာနအသီးသီးမှ ကယ်ဆယ်ရေးပစ္စည်းများ ပို့ဆောင်ပေးမှုမှတ်တမ်း |

ရခိုင်ပြည်နယ်သို့(၁၄-၅-၂၀၂၃)ရက်နေ့တွင် ဝင်ရောက်တိုက်ခတ်ခဲ့သောမိုခါမုန်တိုင်းဒဏ်ကြောင့်ပျက်စီးဆုံးရှုံးမှုများ ဖြစ်ပွားခဲ့ရသည့် မုန်တိုင်းဒဏ်သင့်ဒေသများသို့ ကယ်ဆယ်ရေးနှင့်ပြန်လည်ထူထောင်ရေးလုပ်ငန်းများဆောင်ရွက်နိုင်... |

May 29, 2023 |

2023 | May |

|

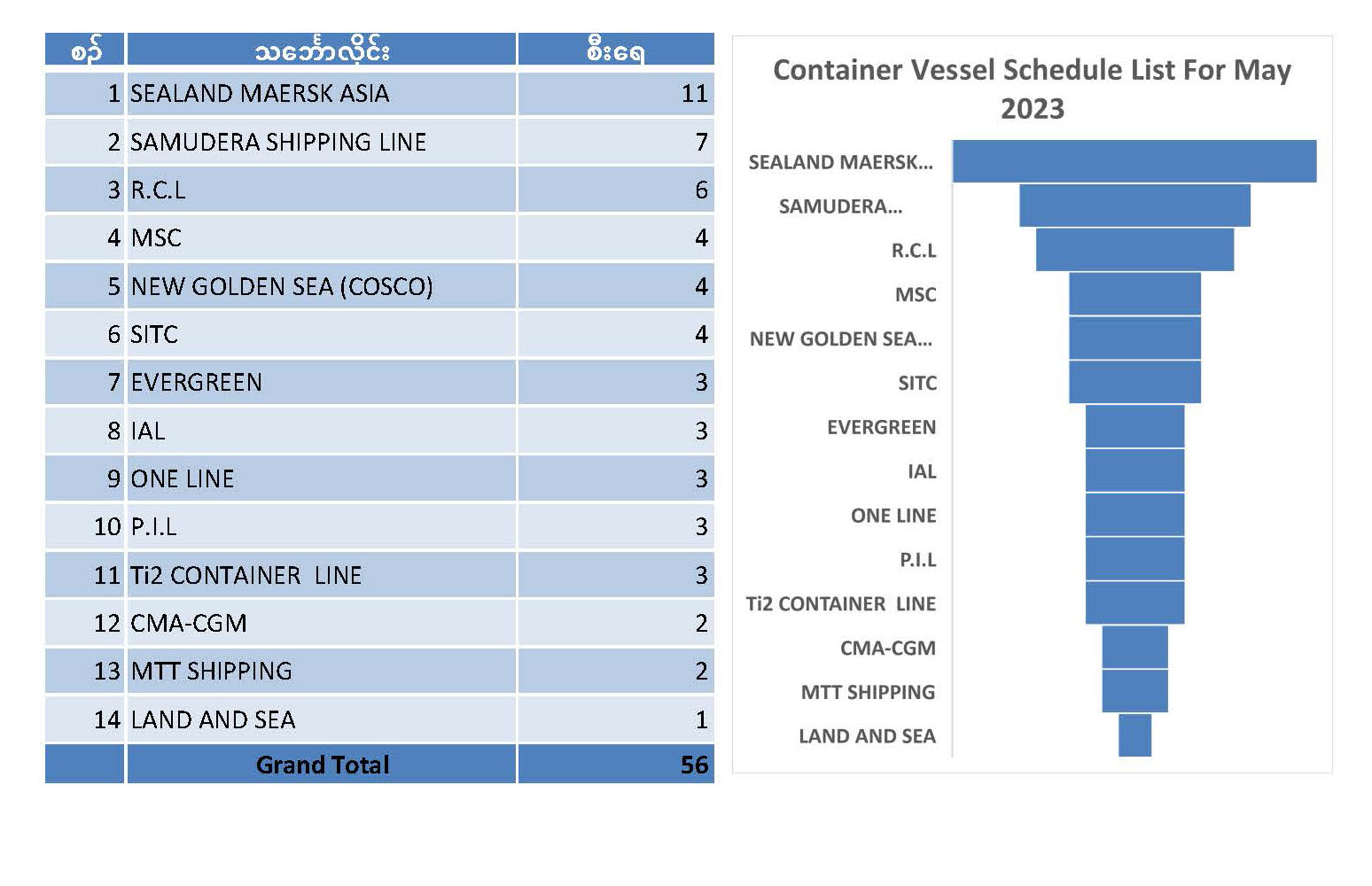

၂၀၂၃ ခုနှစ်၊ ဇွန်လအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်တင်... |

May 29, 2023 |

2023 | May |

|

၂၀၂၃ ခုနှစ်၊ မေလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

April 28, 2023 |

2023 | Apr |

|

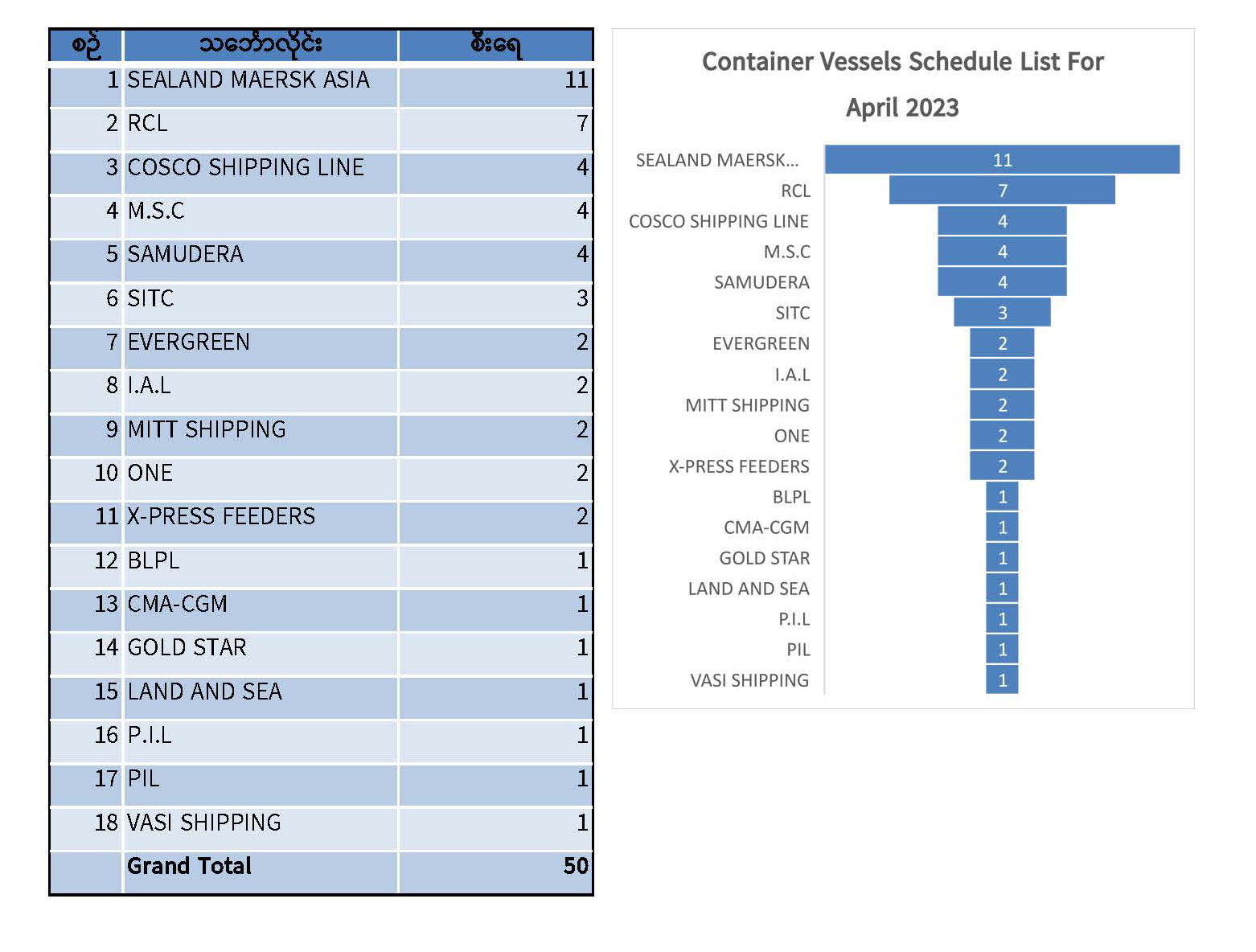

၂၀၂၃ ခုနှစ်၊ ဧပြီလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

March 29, 2023 |

2023 | Mar |

|

၂၀၂၃ ခုနှစ်၊ မတ်လအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

February 27, 2023 |

2023 | Feb |

|

Safety Induction Training -(1/2023) သင်တန်းဖွင့်လှစ်ခြင်း |

လုပ်ငန်းခွင်ဘေးအန္တရာယ်ကင်းရှင်းရေး၊ လုပ်ငန်းခွင်သုံး ကာကွယ်ရေးပစ္စည်းများ မှန်ကန်စွာသုံးစွဲခြင်းနှင့် ဆိပ်ကမ်း... |

February 13, 2023 |

2023 | Feb |

|

၂၀၂၃ ခုနှစ်၊ ဖေဖေါ်ဝါရီလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်... |

Janauary 31, 2023 |

2023 | Jan |

|

၂၀၂၃ ခုနှစ်၊ ဇန်နဝါရီလအတွက် ကုန်သေတ္တာတင် သင်္ဘောစာရင်း |

ပို့ကုန်များ တိုးမြှင့်တင်ပို့နိုင်ရေးအတွက်လည်းကောင်း၊ ပြည်တွင်းလိုအပ်ချက်အရ သွင်းကုန်များလည်း တိုးမြှင့်တင်သွင်းနိုင်ရန်အတွက်... |

Janauary 19, 2023 |

2023 | Jan |

|

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင် ဌာနအကြီးအကဲနှင့် ဝန်ထမ်းများ တွေ့ဆုံဆွေးနွေးဆန္ဒဖေါ်ထုတ်ပွဲ အခမ်းအနား ကျင်းပပြုလုပ်ခြင်း |

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်(ရုံးချုပ်)တွင် ဌာနအကြီးအကဲနှင့်ဝန်ထမ်းများ တွေ့ဆုံဆွေးနွေးဆန္ဒ ဖေါ်ထုတ်ပွဲအခမ်းအနားအား ၂၀၂၃ခုနှစ်၊... |

Janauary 19, 2023 |

2023 | Jan |

|

မြန်မာ့ပို့ကုန် ဆန်နှင့် ဆန်ထွက်ပစ္စည်းများကို ဆူးလေဆိပ်ကမ်းတံတားများမှ ဥရောပနှင့် အာဖရိကနိုင်ငံ များသို့ ဝမ်းပုံစနစ်ဖြင့် တင်ပို့ခြင်း |

ရန်ကုန် ဇွန် ၂၃ မြန်မာနိုင်ငံ၏ အဓိက... |

no 27, 2022 |

2022 | Jun |

|

|

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင် ဌာနအကြီးအကဲနှင့် ဝန်ထမ်းများ တွေ့ဆုံဆွေးနွေးဆန္ဒဖေါ်ထုတ်ပွဲ အခမ်းအနား ကျင်းပပြုလုပ်ခြင်း |

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်(ရုံးချုပ်)တွင် ဌာနအကြီးအကဲနှင့်ဝန်ထမ်းများ တွေ့ဆုံဆွေးနွေးဆန္ဒ ဖေါ်ထုတ်ပွဲအခမ်းအနားအား ၂၀၂၂ခုနှစ်၊... |

May 25, 2022 |

2022 | May |

|

MV.Express Argentina ကုန်သေတ္တာတင်သင်္ဘောကြီး Maiden Voyage အဖြစ် စတင်ဝင်ရောက်လာခြင်း |

Sealand Maersk ၏ MV.Express Argentina... |

May 20, 2022 |

2022 | May |

|

ကွန်ပျူတာအသုံးချ ရုံးသုံးပရိုဂရမ် ကျွမ်းကျင်မှု မွမ်းမံသင်တန်း အမှတ်စဉ် (၁/၂၀၂၂) သင်တန်းဆင်းပွဲ |

ကွန်ပျူတာအသုံးချ ရုံးသုံးပရိုဂရမ်ကျွမ်းကျင်မှု မွမ်းမံသင်တန်းအမှတ်စဉ်(၁/၂၀၂၂)သင်တန်းဆင်းပွဲနှင့် သင်တန်းဆင်းအောင်လက်မှတ် ပေးအပ်ခြင်းအခမ်းအနားသို့... |

May 3, 2022 |

2022 | May |

|

5000 BHP, 65 BPT, 34M, ASD Tug တွန်း/ဆွဲရေယာဉ်အသစ် (၂)စီး ရန်ကုန်ဆိပ်ကမ်းသို့ ရောက်ရှိခြင်း |

"ဆိပ်ကမ်းဝန်ဆောင်မှုလုပ်ငန်းနှင့် ရေကြောင်းဆိုင်ရာ ဘေးကင်းလုံခြုံမှု ပိုမိုကောင်းမွန်စေရေး အတွက်... |

August 19, 2021 |

2021 | Aug |

|

ရန်ကုန်ဆိပ်ကမ်းတွင် ကိုဗစ်-၁၉ ရောဂါ တာဆီးကာကွယ် ထိန်းချုပ်နိုင်ရေးအတွက် လိုက်နာကျင့်သုံးဆောင်ရွက်လျက်ရှိသည့်အစီအမံများ |

ရန်ကုန်ဆိပ်ကမ်းသို့ ဝင်ရောက်လာမည့် အပြည်ပြည်ဆိုင်ရာ ကုန်သွယ်သင်္ဘောကြီးများကို ဆိပ်ကမ်းသို့မဝင်ရောက်မီ... |

August 10, 2021 |

2021 | Aug |

|

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်နှင့် ဆိပ်ကမ်းတံတားများမှ ပိတ်ရက်မရှိ ဆောင်ရွက်ပေးလျက်ရှိခြင်း |

ယခုအခါမှာ နိုင်ငံတော်အနေဖြင့် ကိုဗစ်-၁၉ ရောဂါ ကူးစက်ပြန့်ပွားမှုကို... |

August 7, 2021 |

2021 | Aug |

|

အများပြည်သူရုံးပိတ်ရက်တွင် ကုန်ပစ္စည်းများ ဆိပ်ကမ်းမှ ထုတ်ယူနိုင်ရေးအတွက် ပိတ်ရက်မရှိ ဆောင်ရွက်ပေးသွားမည်ဖြစ်ကြောင်း အသိပေးကြေညာခြင်း |

နိုင်ငံတော်အနေဖြင့် ကိုဗစ်-၁၉ ရော ကူးစက်ပြန့်ပွားမှုကို ပိုမိုထိရောက်စွာ... |

August 2, 2021 |

2021 | Aug |

|

ဆေးနှင့်ဆေးပစ္စည်းများတင်သွင်းသူများသို့ အသိပေးကြေညာချက် |

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်၊ ကိုယ်စားလှယ်လုပ်ငန်းဌာနသည်၊ ပြည်ပမှ ပင်လယ်ရေကြောင်းဖြင့် တင်သွင်းလာသည့်... |

July 26, 2021 |

2021 | Jul |

|

ဆေးနှင့်ဆေးပစ္စည်းများအား ဆိပ်ကမ်းတံတားများမှ အမြန်ဆုံးထုတ်ပေးလျက်ရှိခြင်း |

"ပင်လယ်ရေကြောင်းမှတစ်ဆင့် ကုန်သေတ္တာဖြင့်တင်သွင်းလာသည့်ဆေးနှင့်ဆေးပစ္စည်းများအား ဆိပ်ကမ်းတံတားများမှ အမြန်ဆုံးထုတ်ပေးလျက်ရှိခြင်း" ယခုအခါ... |

July 26, 2021 |

2021 | Jul |

|

အောက်ဆီဂျင်အိုးများ လက်ရှိ ဖြန့်ဖြူးနေမှု အခြေအနေ |

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်၊ စက်မှုအင်ဂျင်နီယာဌာန၊ သိမ်ဖြူသင်္ဘောကျင်းရှိ အောက်ဆီဂျင်စက်ရုံ အနေဖြင့်... |

July 12, 2021 |

2021 | Jul |

|

နိုင်ငံတော်နှင့် ပြည်သူများအတွက် လိုအပ်လျှက်ရှိသည့် အောက်ဆီဂျင်အိုးများ ဖြန့်ဖြူးပေးခြင်း |

မြန်မာ့ဆိပ်ကမ်းအာဏာပိုင်၊ စက်မှုအင်ဂျင်နီယာဌာန၊ သိမ်ဖြူသင်္ဘောကျင်းရှိ အောက်ဆီဂျင် စက်ရုံသည်... |

July 9, 2021 |

2021 | Jul |

|

ကုန်သေတ္တာတင်သင်္ဘောများဝင်ရောက်မှုနှင့် ပို့ကုန်ကုန်သေတ္တာလိုအပ်ချက်အတွက် လုပ်ငန်းညှိနှိုင်းအစည်းအဝေး ကျင်းပခြင်း |

ရန်ကုန် ဧပြီ ၂၂ အပြည်ပြည်ဆိုင်ရာ ကုန်သွယ်မှု၊... |

April 28, 2021 |

2021 | Apr |

|

MV Expert Carried Steel 38,782 Metric Tons for Construction Called to Yangon Port and Berthed at MITT, Thilawa |

Thilawa 24 April Along with... |

April 28, 2021 |

2021 | Apr |

|

မြေတူးမြေခံ ရေယာဉ်များ အသစ်တည်ဆောက်ခြင်း |

နိုင်ငံတကာနှင့်ကုန်သွယ်မှု ပိုမိုတိုးတက်များပြားလာသည်နှင့်အမျှ ပင်လယ်ရေကြောင်းဖြင့် ကူးသန်း ရောင်းဝယ်မှု... |

March 25, 2021 |

2021 | Mar |

|

Announcement |

1. Myanma Port Authority (MPA)... |

March 25, 2021 |

2021 | Mar |

|

Second trip of Yangon-Cocokyun |

At October 18, 3:00 pm,... |

October 22, 2020 |

2020 | Oct |

|

Ureas Discharging of MV.HAI DUOWG-36 at SPW (7) Wharf |

At Sule Port No. (7)... |

February 1, 2019 |

2019 | Feb |

|

Northeast Asia Logistics Information Service Network (NEAL-NET) |

ကမ္ဘာ့ရေကြောင်းအဖွဲ့ချုပ်မှ ကျွမ်းကျင်ပညာရှင်နှစ်ဦးအနေဖြင့် မြန်မာနိုင်ငံသို့ လာရောက်ပြီး Northeast... |

April 4, 2017 |

2017 | Apr |

|

|

Study on Template Transaction Documents under PPP Contracts |

ဆိပ်ကမ်း ကဏ္ဍတွင် ပုဂ္ဂလိက ရင်းနှီးမြှုပ်နှံမှုများ ဆောင်ရွက်ရာတွင်... |

February 9, 2017 |

2017 | Feb |

|

Collaboration between European companies and Myanma Port Authorities |

Representatives of the EuroCham Myanmar... |

September 28, 2016 |

2016 | Sep |

|

(LOC) Letter of Cooperation |

Port and Harbours Bureau, Ministry... |

September 13, 2016 |

2016 | Sep |

25.7 MT Cargo Handling Volume

1.09 TEU Container Handling Volume

1,258 Vessel Call

$26.8 B Trade by Value

Myanmar International Terminals Thilawa (MITT) is a multi-purpose container terminal located at Thilawa near the mouth of the Yangon River. The terminal offers a comprehensive range of safe, efficient and productive services to the shipping industry 24 hours a day seven days a week.

Go to Website